You’ve been asked to cut your marketing budget. Now what?

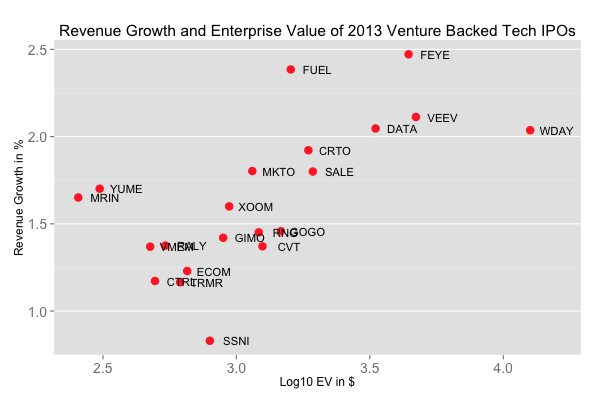

Unicorpses. Layoffs. Bursting bubbles. Winter is coming. Every day there’s a new story on the 2016 techpocalypse. Having lived through the 2000 dot com crash, this is nothing like it. But something has changed, so let’s start with a quick recap of how we got here. Starting in late 2012, tech companies began to raise massive funding rounds to chase growth. Here’s a chart put together by Tom Tunguz showing how the stock market once rewarded high growth tech companies:

Most of these companies are SaaS, which requires access to a huge amount of funding to run the business. Back in 2013 and 2014, money was plentiful. Private SaaS companies were able to raise hundreds of millions of dollars on the back of business plans that promised huge growth. And the market was so hot that non traditional investors — people like Wellington Management and Fidelity — jumped into the private company financing mix, often at much higher valuations than traditional venture investors were paying. The most publicized example is Box, who grew revenue 110% in the year prior to their IPO but famously spent about 137% of its revenue in sales in marketing (over $170m!) to fuel the massive growth. The idea was that the SaaS unit economics of Box would eventually lead to a highly profitable business, where Box would a) “Land and expand” to keep net renewal rates well above 100% b) Lower sales and marketing costs to a more reasonable 35–40% of revenue range. While Box had to delay their IPO, ultimately they spun a compelling enough story to close nearly 70% higher on their first day of trading at close to a $3b valuation. But as we’ve learned in early 2016, markets go up, and markets go down. Box now trades at less than its IPO price, even though it continues to grow. Nearly all of the tech IPOs from the past couple of years are currently trading below their IPO price. Private company valuation have taken an even bigger hit as they had further to fall due to the unusually high multiples they received in the recent past. Today, investors are no longer funding the grow-at-all-costs mentality of the past few years. They now expect companies to actually make money, or at least be able to paint a clear path to cash flow breakeven. While well funded public and private companies can hunker down and invest for the long term, not every company has a war chest of cash on the balance sheet. So CEOs who once had access to unlimited private financing and/or a welcoming IPO market now must operate within the constraint of a reasonable burn rate… slowing hiring, cutting expenses, increasing gross margins, selling more… And yes, cutting marketing programs. Marketing programs are one of the few levers CEOs can quickly scale up and down. If you’ve been asked to look at cutting your marketing budget, here’s where’s to start: Thank your CEO. CEOs are constantly faced with impossibly difficult decisions. Telling a high performing organization that they need to scale back can damage team morale. But as Heidi Roizen of venture firm DJF puts it:

You know what hurts morale even more than cost- cutting and layoffs? Going out of business.

Be transparent with your team. You can’t hide smaller budgets from your team, so include them in the budgeting process and help them understand the new constraints. And maybe send them this post :) Scale with brainpower, not budget. Rapidly growing marketing budgets creates bad behavior. People begin to equate their value to the company with the size of their budget, and makes it easier to spend on programs with questionable ROI. Pragmatic cuts to the marketing budget will help bring great clarity and focus back to your team, and eliminate the fiefdoms that sometimes form around budgets. Most importantly, reduced budgets are a chance for your team to apply their brainpower, through developing new approaches, responsibilities and skills that might have been hidden by a bloated budget. Eliminate the stuff you won’t measure. Marketing has gotten much better at measuring our impact on the business, and we’re pretty good at looking at how marketing spend across different channels drives leads, pipeline, and bookings. But there are still questionable “brand” investments we make that we’re not great at measuring — like PR. Jason Lemkin of Storm Ventures wrote a great post on how he measured PR at Echosign. If you can’t commit to measuring your brand investments, then scale them way back. Or put much more effort into assessing their impact on the business and hold yourself accountable. Stop buying leads. Joe Chernov of InsightSquared recently published a fantastic article on the rise of account-based marketing and marketing’s unhealthy obsession with the MQL. Many marketing departments operate on a spreadsheet model that sets MQL targets based on revenue goals and historical conversion metrics. That’s great, you should absolutely create that model. But your spreadsheet model is going to show that you need to create an unsustainable number of MQLs each quarter. This puts pressure on marketing to run expensive cost-per-lead programs to hit the lead commit. These less qualified leads then make your conversion rates worse, leading to your spreadsheet model telling you that you need even more leads next quarter. This approach is broken. As Joe puts it:

Sales teams don’t need a torrent of minimally qualified leads; they need air cover.

Investing in account-based marketing is potentially a much more effective way for you to reach the companies who can actually buy your product. And it will help you better align sales and marketing by focusing efforts on a specific set of companies. Take a hard look at events. Events can be difficult to scale back because they are often planned months or years in advance. But if you look closely, I bet you’ll find ways to cut back 10–20% from your budget without impacting the quality. People come to events to learn and network, so focus on the quality of your content and assembling the right people.